This article deepens one element within the broader decision framework: "Is This Deal Right for You? A Five-Gate Decision Framework for Central Texas Rental Investors."

That framework addresses the full acquisition decision. This analysis focuses on a single failure point—applying the wrong valuation methodology to a property type and distorting buy, hold, or refinance outcomes as a result.

Executive Snapshot

Objective:

Determine whether you are applying the right valuation methodology and metrics to the property type you are analyzing.

Key Takeaways:

Single-family homes are valued primarily by comparable sales; income performance does not directly drive appraised value

Properties with 2-4 units exist in a transitional zone requiring dual-lens analysis—both comparable sales and income approach matter

Properties with 5+ units are typically valued by income performance; operational improvements can create immediate value

The shift from 4 to 5 units generally triggers commercial financing, different underwriting standards, and a fundamentally different value driver

Applying the wrong valuation framework to a property type creates misalignment with lenders, appraisers, and future buyers

Best Use Case:

Residential property owners evaluating acquisition, refinance, or hold decisions across different asset classes need to understand which metrics actually influence value for their property type.

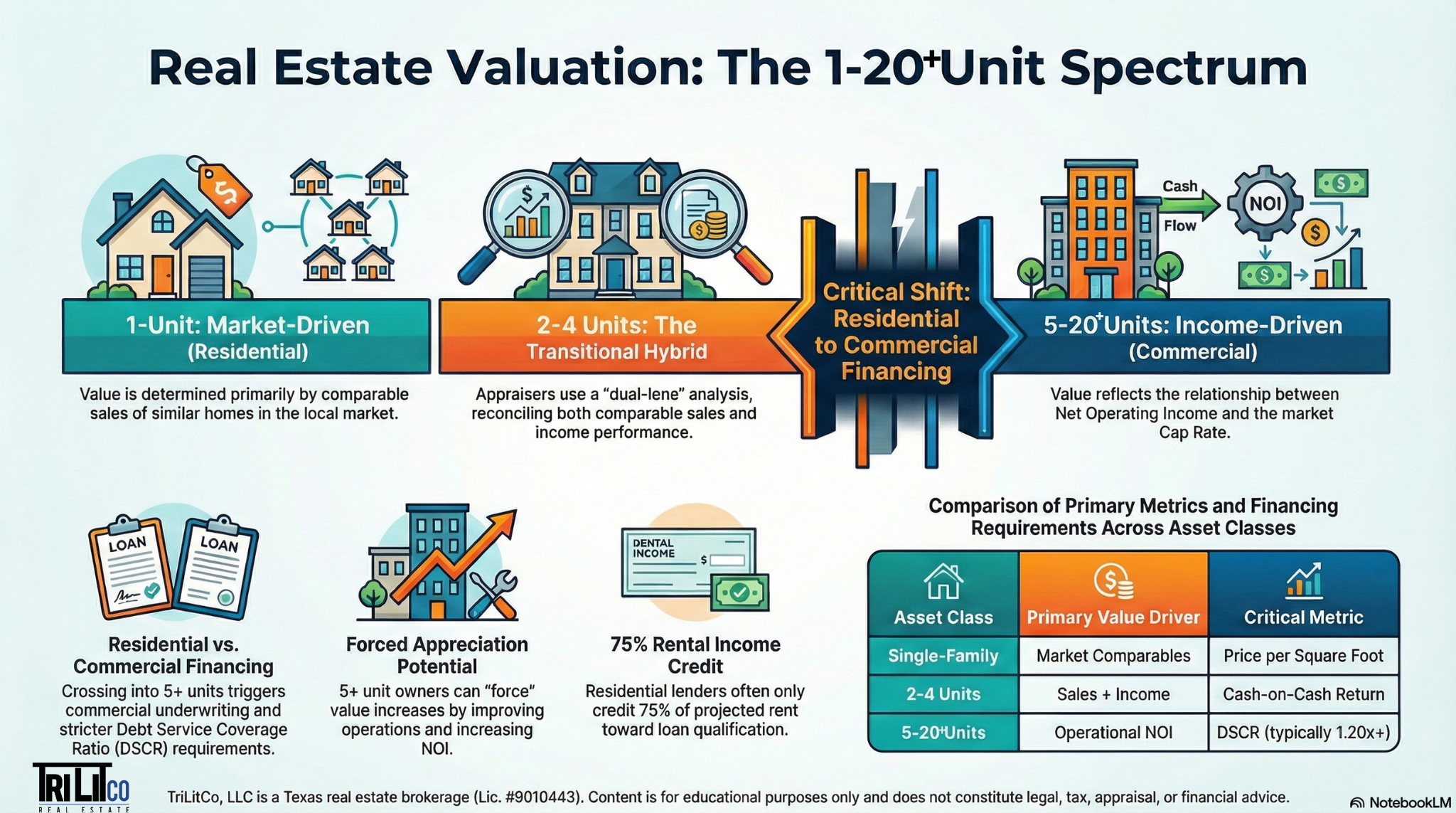

Why Valuation Approach Depends on Property Type

Real estate valuation is not universal.

A single-family rental, a fourplex, and a 12-unit building may all generate rental income, but they are valued using fundamentally different methodologies.

The distinction matters because lenders underwrite financing based on property classification, appraisers weight different approaches depending on unit count, buyers evaluate properties through different lenses, and exit strategy depends on which valuation method the next buyer will use.

The most significant threshold is typically the transition from 4 to 5 units.

While this standard is widely recognized—especially for Fannie Mae and Freddie Mac residential financing programs that cap at 1-4 units—classification may vary based on lender guidelines, local zoning, or property-specific characteristics.

For most residential rental owners, crossing from 4 to 5 units means transitioning from residential into commercial classification, which changes financing options, underwriting standards, and the primary driver of value.

Single-Family Homes

Market-Driven Valuation

Single-family rental properties are valued primarily through the sales comparison approach.

An appraiser identifies recently sold properties that are similar in location, size, condition, and features, then adjusts for differences to estimate value.

Income performance—rent amount, vacancy rate, operating efficiency—provides context but does not directly establish appraised value.

If comparable homes in the neighborhood sold for $400,000, a rental generating strong cash flow will not appraise for $450,000 based on that income alone.

This creates a constraint: you cannot force appreciation on a single-family rental by improving operations or raising rent.

Value moves with the market. Renovations add value only if the market recognizes and pays for those improvements through higher comparable sales.

Financing Context

Single-family investment properties (1-4 units) qualify for residential financing through Fannie Mae and Freddie Mac programs.

Lenders underwrite based on the borrower's income and creditworthiness.

Many lenders apply a rental income credit—often around 75% of projected rental income—to account for vacancy and operational contingencies, though specific guidelines vary by lender and loan program.

Down payment requirements typically range from 15-25% for investment properties, compared to 20-30% for commercial loans on 5+ unit buildings.

2-4 Unit Properties

The Transitional Zone

Duplexes, triplexes, and fourplexes occupy a hybrid space.

They remain within the residential financing classification (1-4 units) but begin to function as income-producing assets in ways that single-family homes do not.

Appraisers use dual-lens analysis: the sales comparison approach examines what similar 2-4 unit properties sold for, while the income approach evaluates the property's ability to generate net operating income relative to its price.

Both approaches must reconcile.

If comparable sales suggest a duplex is worth $500,000 but the income approach suggests $450,000, the appraiser must determine which approach carries more weight given the property's characteristics and the local market.

This creates both complexity and opportunity.

A 2-4 unit property that performs well operationally may support a higher valuation if income-focused buyers dominate the market. Conversely, a property priced based on strong comparable sales may not justify its price when income performance is weak.

Buyer Pool Considerations

The 2-4 unit category attracts two distinct buyer types: owner-occupants using FHA or conventional financing, who may prioritize livability and location over pure investment returns, and investors focused on cash flow, who weight income performance more heavily.

This creates a flexible but uncertain exit strategy.

The next buyer may use a different valuation framework than you did.

5-20+ Unit Properties

Income-Driven Valuation

Once a property reaches 5 units, it is typically classified as commercial real estate.

The primary valuation method shifts to the income approach.

However, this threshold is not absolute.

While the 4-to-5 unit distinction is the most common classification standard—particularly for Fannie Mae and Freddie Mac residential financing, which caps eligibility at 1-4 units—some lenders and loan programs may apply commercial underwriting standards at different thresholds.

Additionally, local zoning regulations, mixed-use features, and property characteristics may influence classification regardless of unit count.

For Central Texas residential rental owners evaluating properties in the 1-20 unit range, the practical takeaway is this: the shift from 4 to 5 units generally triggers commercial financing and income-driven valuation, but confirm classification and financing eligibility with your lender before proceeding with analysis.

Value reflects the relationship between net operating income and the market's required return.

Net operating income represents gross operating income less operating expenses—excluding mortgage payments, capital expenditures, and depreciation.

Operating expenses include property taxes, insurance, utilities (if owner-paid), repairs, management fees, and administrative costs.

The cap rate—often summarized as NOI ÷ property value—expresses the market's required return for a property of this type, condition, and location, not a decision rule to be optimized in isolation.

Cap rates vary by asset quality, location, and market conditions.

Lower cap rates correspond to higher prices (typically lower-risk, higher-demand markets); higher cap rates correspond to lower prices (typically higher-risk or income-focused markets).

Forced Appreciation Becomes Possible

Unlike single-family and 2-4 unit properties, income-valued properties allow for forced appreciation.

The valuation relationship mathematically implies that increasing NOI by $10,000 annually in a market with a 6% cap rate would suggest a property value increase of approximately $167,000—though actual market recognition depends on buyer perception, transaction execution, and market conditions at time of sale, including whether cap rates remain stable.

Methods to increase NOI include raising rents to market rate, adding income sources such as parking or storage, reducing operating expenses through efficient management, and decreasing vacancy through improved tenant screening and retention.

This creates a fundamentally different ownership model.

Value is no longer dependent solely on market movement—it responds directly to operational performance.

Commercial Financing Requirements

Properties with 5+ units typically require commercial financing.

Loan qualification is based primarily on the property's income, not the borrower's personal income.

Lenders evaluate Debt Service Coverage Ratio (DSCR)—the margin by which property income exceeds required debt service.

Most commercial lenders require a DSCR of at least 1.20x to 1.25x, meaning the property must generate 20-25% more income than is needed to cover the mortgage payment.

Typical commercial loan terms include loan-to-value (LTV) ratios of 65-75%, down payments of 20-30%, loan terms of 5-10 years with balloon payments, and reserve requirements of 6-12 months of operating expenses.

This creates a higher barrier to entry but also aligns financing directly with property performance.

Key Metrics by Asset Class

Different property types require different analytical tools.

For Single-Family Rentals

Price per square foot and comparable sales adjustments are primary.

Cap rate can be calculated but does not drive appraised value.

Gross Rent Multiplier (GRM) provides a rough screening metric—the ratio of property price to gross annual rental income.

However, GRM ignores operating expenses entirely and should not replace cap rate analysis for serious evaluation.

For 2-4 Unit Properties

Both comparable sales and income metrics matter.

Run the analysis through both lenses and identify any significant disconnects.

Key metrics include cap rate (even if not the dominant valuation driver), cash-on-cash return (actual return on invested equity), and operating expense ratio (to assess efficiency).

The dual-lens requirement reflects the dual buyer pool.

For 5-20 Unit Properties

Net operating income and cap rate are primary.

Comparable sales provide a cross-check but do not override income-based valuation.

Additional critical metrics include DSCR (lender qualification threshold), break-even occupancy (minimum occupancy required to cover expenses and debt service), operating expense ratio (operational efficiency benchmark), and price per unit (quick comparison tool, but secondary to income performance).

Cash-on-cash return measures actual return on invested capital and is sensitive to leverage.

Higher leverage increases cash-on-cash return but also increases risk if DSCR margins are thin.

Where Analysis Commonly Breaks Down

Several patterns create valuation misalignment.

Applying Income Metrics to Market-Valued Properties

Calculating cap rate on a single-family rental and expecting it to drive value creates false confidence.

Appraisers and lenders will use comparable sales regardless of income performance.

Using Comparable Sales Logic for Income-Valued Properties

Evaluating a 12-unit building primarily on price per unit without analyzing NOI and cap rate ignores how these properties are actually valued and financed.

Price per unit is a screening metric, not a valuation method.

Underestimating the 4-to-5 Unit Threshold

Treating a 5-unit property like a large fourplex creates financing and valuation misalignment.

The shift to commercial classification is generally abrupt and material for standard agency financing, though owners should confirm classification requirements with their specific lender.

Using Pro Forma Projections to Justify Acquisition Price

Pro forma projections reflect potential future performance after improvements.

Lenders underwrite based on trailing 12-month actual performance.

Paying today's price based on tomorrow's projected income transfers execution risk entirely to the buyer.

If the projected improvements do not materialize, the property may not support its debt service or justify its purchase price.

Ignoring Rental Income Credit Practices

Many lenders apply a rental income credit when qualifying borrowers for 1-4 unit investment properties—typically around 75% of gross rental income to account for vacancy and expenses, though specific practices vary by lender and loan program.

Assuming 100% of rent qualifies creates financing shortfalls.

Confirm your lender's specific underwriting approach before relying on projected rental income for loan qualification.

Stress Scenarios and Sensitivity

Valuation outcomes are sensitive to assumption changes.

Cap Rate Movement

A 1% increase in cap rate (from 6% to 7%) reduces property value by approximately 14% even if NOI remains constant.

Cap rates tend to follow interest rates with a lag.

Rising rates compress values for income properties even when operations remain stable.

Vacancy Increases

A 5% increase in vacancy directly reduces NOI.

For a property generating $200,000 in gross income, a move from 5% to 10% vacancy reduces NOI by $10,000.

At a 6% cap rate, this reduces property value by approximately $167,000.

Expense Increases

Property tax reassessments, insurance premium spikes, and deferred maintenance costs flow directly to NOI reduction.

These expenses are often underestimated in initial projections.

Comparable Sales Collapse

For single-family and 2-4 unit properties, market downturns reduce comparable sales prices regardless of income performance.

A property may cash flow well but lose value if the market declines.

How Financing Constraints Shape Valuation

Valuation analysis is academic if the property cannot qualify for financing at the proposed purchase price.

For 1-4 unit residential properties, lenders underwrite based on borrower income and creditworthiness.

Many lenders apply a rental income credit—typically around 75% of projected rent—though specific practices vary. LTV ratios typically reach 75-85% for investment properties.

For 5+ unit commercial properties, lenders underwrite based primarily on property income.

DSCR must meet minimum thresholds (typically 1.20x-1.25x), and LTV ratios are typically 65-75%. Reserve requirements of 6-12 months are standard.

If a property's NOI cannot support the required DSCR at the purchase price, the deal does not qualify—regardless of what the valuation relationship suggests.

Integrating Valuation Analysis Into Decisions

A structured approach reduces misalignment.

Classify the property. Is this 1-4 units (residential) or 5+ units (commercial)? This determines financing options and primary valuation method. Confirm classification with your lender, as some variation may exist based on property characteristics or loan programs.

Identify the primary valuation approach. Single-family uses sales comparison. 2-4 units use dual-lens. 5+ units use income approach.

Gather appropriate data. For single-family, collect comparable sales. For 2-4 units, collect comparable sales and rent roll. For 5+ units, collect trailing 12-month financials, rent roll, and market cap rates.

Run the numbers through multiple lenses. Calculate value via applicable methods. Calculate key metrics (cap rate, DSCR, cash-on-cash return, break-even occupancy). Identify disconnects between approaches.

Stress test assumptions. Model a 5% vacancy increase, a 1% cap rate increase, and a 1% interest rate increase. Determine whether the deal remains viable under stress.

Align with financing reality. Confirm the property can qualify for financing at the proposed price. Verify DSCR meets lender requirements and reserves are sufficient.

Consider exit strategy. Identify who will buy this property and what valuation approach they will use. Confirm that operational improvements (if planned) will translate to exit value.

When analysis frameworks conflict, prioritize in this order: lender requirements, trailing actual performance, conservative assumptions, then pro forma potential.

Final Considerations

Valuation methodology is not a matter of preference—it is determined by property classification, financing structure, and market convention.

Misalignment between your analysis framework and the framework used by lenders, appraisers, and future buyers creates execution risk.

The transition from 4 to 5 units typically represents the most significant analytical threshold for standard agency financing.

Properties below this threshold are valued primarily by market forces; properties above it are valued primarily by income performance.

While some lender-specific or property-specific variation exists, this remains the dominant classification standard.

Understanding which framework applies to your property type—and which metrics actually influence value—reduces the risk of overpaying, misforecasting returns, or misaligning with financing requirements.

Valuation is the foundation. Financing feasibility, operational execution, and exit strategy build on it.

If the foundation is misaligned, the rest of the analysis compounds the error.

Next Step:

Confirm your current or target property's classification with your lender, then apply the corresponding valuation methodology before proceeding with buy, hold, or refinance analysis.